Market Update March 30th, 2026

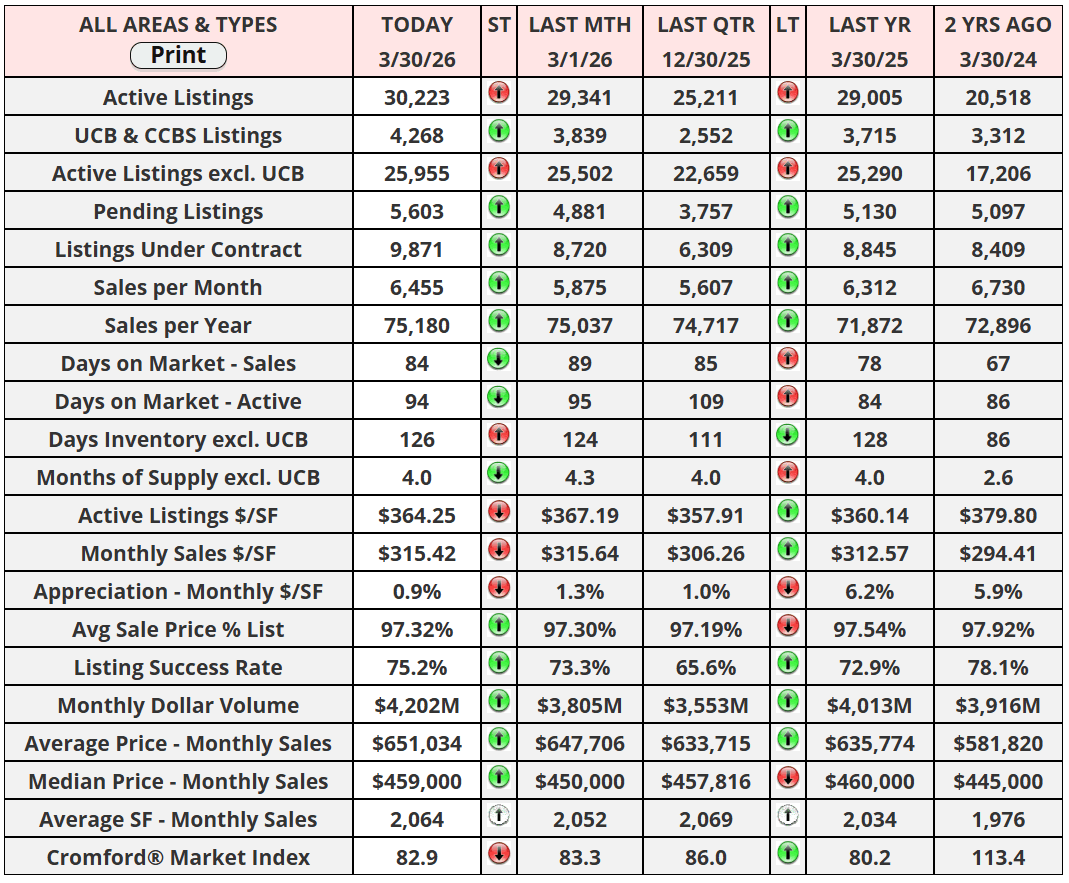

Twelve of the eighteen largest cities in the Phoenix metro are now moving in a direction favorable to sellers, up from eight just two weeks ago and the strongest seller reading we have seen since the start of the year. The average Cromford Market Index climbed 1.7%, a significant acceleration from the 0.2% uptick we saw last week. Perhaps surprisingly, this is happening while mortgage rates have been pushing higher. The 30-year fixed sits around 6.55% after several weeks of increases.

But this is not a runaway seller's market. It is important to keep the broader picture in focus. Of the ten seller's markets, four still carry weak advantages with CMI readings below 120. Six cities remain buyer's markets. Supply continues to climb with active listings (excl. UCB) hitting 25,955, and that upward trend in inventory has not shown signs of peaking. Until it does, the CMI will struggle to move decisively higher. Sellers should take encouragement from the momentum shift, but pricing aggressively based on these early signals would be premature.

On the demand side, listings under contract reached 9,871, up 11.6% compared to the same week last year and marking the fifth consecutive week of outperformance against prior years. Pending listings hit 5,603, up 9.2% year over year. The demand engine is running despite rate headwinds, which speaks to pent-up buyer activity that has been waiting for an entry point. Sales per month came in at 6,455, up 2.3% year over year.

Pricing tells a nuanced story. The average sale price landed at $651,034, up 2.4% year over year, while the median came in at $459,000, essentially flat compared to last year. Monthly dollar volume hit $4.20 billion, up 4.7% year over year. Appreciation has cooled further to 0.9% on a monthly basis, down from 1.0% last week and well below the 6.2% pace from this time last year. That deceleration in appreciation is worth watching. Prices are not falling, but the growth rate is flattening in a way that signals the market is looking for equilibrium rather than another leg up.

Goodyear led the charge this week with a 16% CMI move in favor of sellers, followed by Tempe at 11% and Maricopa at 9%. On the other side, Gilbert dropped 10% and Cave Creek dropped 10% toward buyers, making them the two most buyer-favorable cities for the second consecutive week. Chandler continues to hold the top spot at 154.5, the only city above 150.

Here is the honest read: the seller momentum is real, but it is being fueled by demand strength, not by supply tightening. That makes it fragile. The Iran conflict is the biggest wildcard hanging over this market right now. Since U.S. and Israeli strikes began on February 28, mortgage rates have jumped from 5.99% to around 6.55% as oil surged past $100 per barrel and the Strait of Hormuz disruption rattled global markets. Gas prices are up 32% in three weeks to nearly $4 a gallon nationally, squeezing household budgets heading into the critical spring selling season. The average household is projected to spend an additional $740 on gas this year because of the oil price shock. The Fed held rates steady at 3.50%-3.75% at its March meeting, raised its inflation forecast to 2.7%, and signaled only one possible cut this year. That is a stark reversal from the two to three cuts markets had priced in back in January. Fed Chair Powell acknowledged it is "too soon to know" the full economic impact. Meanwhile, tariff inflation continues to compound the picture, making it harder for the Fed to justify easing. KB Home has already lowered its full-year forecast citing consumer uncertainty from the conflict. So far, Phoenix demand has been resilient despite all of this. But the longer these headwinds persist, the more pressure builds on buyer confidence, affordability, and transaction volume. We are at the inflection point, not past it!

"In the middle of difficulty lies opportunity." - Albert Einstein

Have a great week, everyone!